Mortgage Rates Near Historic Lows!

Have you decided that 2020 will be the year that you upgrade or change your residence?

If you are like most people, you plan to put your house on the market in the “spring.” Spring begins on March 19 this year. This makes sense since winter weather is unpredictable. Who would looks at houses in bad weather?

Because I have been actively involved in the Metro real estate market since 1986, a curious phenomenon takes place in the winter – houses sell, quickly. In fact, inventory that had not sold the prior summer and autumn sell in January and February. along with the new listings. Another interesting observation is that houses that listed for sale in April and onward, took longer to sell.

Since properties sell in January, February, and March, this also means that some of the best properties will also sell before “spring.”

While this might seem soon, if you are serious about your new home, sooner will be in your best interest.

We are prepared to help you have a great real estate experience. The first step – give us a call and let’s discuss your hopes and plans.

For many people condominium ownership is the gateway to real estate ownership. Stringent FHA guidelines have hampered many people from being able to purchase a home. The much awaited revised guidelines provide enhanced flexibility in three key aspects as follow:

The new guidelines will provide flexibilities for buyers and sellers to be able to increase homeownership to more people. Additionally, more units will be available for buyers to choose from, thus widening the real estate inventory opportunities.

Have you been priced out of the market or been unable to find and eligible condo to buy? With newly reduced interest rates and more flexible guidelines, NOW is your time! CAll TODAY 703-624-8333 or visit our website – http://www.POTPHOMES.com and contact the agent of your choice directly.

The full rule for single-family condo financing was published in the Federal Register on Aug. 15, 2019, and available online at https://federalregister.gov/d/2019-17213, and on govinfo.gov.

As expected, and going against the wishes of some, the Fed increased policy rates by a quarter percent at their December meeting. This is the fourth hike this year and the ninth since 2015. Previously, the benchmark rate was kept at a record low for seven years.

What does an increase mean?

• It could cause banks to increase their “prime rates,” which are often used to calculate interest on consumer products like credit cards, private student loans, and home equity lines of credit (HELOCs). Adjustable Rate Mortgages (ARMs) may be directly impacted as well.

• Fixed mortgages are typically based on long-term rates, which are not directly affected by Fed rate changes. However, Fed policy does influence mortgage rates, which can rise in anticipation of future Fed action. There are exceptions, yet home loan rates will typically follow overall interest rate trends over time.

Here’s something new:

Officials initially projected three additional Fed rate hikes for 2019, but that number dropped to two. Fed members say they will continue monitoring economic data to make future decisions.

In this volatile economic season, please reach out to us to discuss how all of this might affect your real estate decisions.

NOTE: this article was graciously shared by Mark Ferguson, Senior Loan Officer, MVB Mortgage.

Amazon recently announced their selection of Crystal City – Arlington, VA as the future home of one of their two additional headquarters. The news was met with delight and trepidation by the Northern Virginia and general Metro community.

Homeowners, naturally, had visions of dollar bills dancing through their heads as they anticipated accelerated appreciation of their homes. Commuters feared traffic congestion beyond present levels. Developers envisioned windfall profits.

Increased employment, greater appreciation, and profits, oh my!

A few facts (as presented by NVAR and their panel of experts during their December 12 presentation on the “Amazon Effect” at George Mason Business):

The six experts all warned to guard against the “hype wave” and to be strategic.

The KEY: this will be a 16 year project, which according to the experts, will be absorbed within ordinary area growth.

The question asked almost daily, “How will this event impact our real estate value?” is best answered by, “The impact happened at the anticipation phase.”

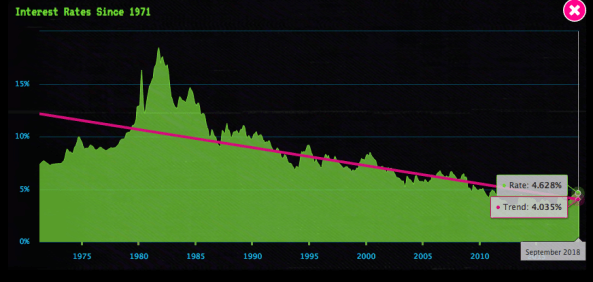

Click on the link to see how interest rates have affected housing over the decades .

.

What exactly does it mean to you when your mortgage has been “sold?”

The sale of mortgage “paper” and/or servicing is common practice.

Federal law requires that the outgoing mortgage holder must send you in writing, notification of the sale and provide you with the new company’s contact information. The new company must also send you in writing their “welcome” letter and provide you with clear instructions on how and where to pay your mortgage. To learn more, visit http://www.consumerfinance.gov/askcfpb/215/what-happens-if-my-mortgage-servicer-changes-what-do-i-do.html

So what could possibly go wrong? Realize that many of the servicing agents are not located in the United States; data from the loan package is often manually entered into a new database; and escrow accounts can slip into an abyss. Because you, the mortgagor, are ultimately responsible for your mortgage, taxes, and insurance; you must be vigilant.

The subject of escrows held by a lender (or lender’s servicing company) has been tested in court and it has been determined that “when the lender holds escrow funds for property tax payments, a fiduciary duty exists.” This is a very important decision inasmuch as the lender has the obligation to you to pay all taxes and insurance (should they be collecting for that as well) in a timely manner.

A client recently contacted us for help sorting out the sale of their mortgage and getting their taxes paid on time. After two months of phone calls, and several emails, their property taxes were finally paid. However, the County and Town tax records now show that late payment interest and penalty fees had been levied and received. This indication is not on the servicer’s record, it is on the homeowner’s record.

What’s a homeowner to do?”

If you have any questions, you can always contact us.

Most art is delicate and potentially fragile. How you handle your art during and after a move can determine your future enjoyment of the piece(s) and their value.

For the past 20 years, we had hung a beautiful limited edition print on a wall in the basement. This was mostly because the wall was large enough for the piece and because we had tired of it in our every day living space. Several says ago, during a discussion about art and artists, I took a close look at the piece. I discovered some tiny black dots on the Japon paper.

The print, framed by conservation standards, was installed on an exterior below-grade wall. Regardless of the finish level of the wall, the structural cinder block must get moisture that was trapped by the art. SO now, mildew in the paper of a pretty valuable piece of art.

Naturally, my first thought was to contact an art conservator and organize its restoration. This is where a whole new world of art services came alive. Art conservators do not conserve paper. They restore/clean paintings – oils, linen, canvas, and the like. Paper restorers handle prints on paper. Yes, the same experts that restore books, restore art prints.

You know that some art will appreciate over time. We just never know what piece(s) might become valuable in the future. Most people buy art for its aesthetic value and not so much for investment. However, sometimes artists gain in notoriety and if their work survives long enough in good condition, the value could increase.

If you want to both enjoy and preserve your art, handle it carefully and install it with consideration of potential moisture (even condensation that forms inside a sealed frame).

Should you need a conservator of antiques, paintings or paper, we have now amassed a list of conservators who can help and/or direct you to solving your. Some have performed work for us personally, others have been recommended and have significant credentials. Give us a call and we will gladly share our list.

The news about the Federal Reserve and the Fed Funds Rate is often touted as a reason to anticipate increased mortgage interest rates. As with much of the media, “news” can be manipulated to stimulate emotional reactions from joy to fear. The fear in this case would be of increasing interest rates.

What actually happens when the “Fed” raises the ‘Fed Funds Rate’? Well, those rates apply to funds that banks borrow from the Federal Reserve for periods less than 90 days, but longer than one day. Raising the rate by .25% on banks does not necessarily affect mortgage rates at all.

The Federal Reserve serves an important function in the United States – insuring deposits from bank default (within established limits) and monitoring and controlling monetary policy in hopes of maintain a stable economy with limited fluctuation. Monetary policy is complex and very carefully monitored by financial institutions and corporations.

Borrowing money to purchase a home typically falls under the term, mortgage. Mortgages consist of two components – principal and interest. While we all know about principal, the interest component often seems like hocus pocus in a black box. Interest is the amount that lenders charge for the privilege of lending money.

Because mortgages are typically a long-term commitment on the part of the lender, economic projections are used to set prevailing interest rates. Lenders look at the risk of inflation and the potential opportunity cost of leaving their money at a set rate for a prolonged period of time.

Mortgage interest rates are typically affected by long term bond yields and the 10-year Treasury bills. Obviously, every aspect of the monetary markets trickle down to affect interest rates, however, mortgage rates are not as sensitive to the “Fed Rate” as they are to the Treasuries or Bond Yields.

Why does this information matter to you? You are barraged by offers, threats, and disinformation to act “quickly” to refinance or to buy now. Yet, the reality is that mortgage markets are more insulated than reflected in the news.

However . . . depending on your sensitivity to rate fluctuations, a small move in mortgage interest can affect mortgage qualification. The best solution is to work with a knowledgeable lender who can guide you with correct information with which you can make good decisions.

If you are thinking of buying or refinancing, we have an excellent list of lenders who have worked for our clients who produce loans on time and on budget. Call us today.