Many people design their homes with a future buyer in mind. They choose neutrals whether or not they like them. Yes, it is safe. It might not offend anyone. They live cautiously, as if tenants in their own homes.

As a first-time homebuyer, I made different decisions. I chose to decorate our home. I did not ‘stage’ it. I did not neutralize it. I decorated it to our taste and expectations. It was not expensive, simply lovely.

I was warned repeatedly. “Nobody will buy this when you want to sell.” ‘They’ were wrong. Not only did my homes sell, they sold quickly and for top values. Even when two of my two-story foyer walls were enameled in hunter green.

Why? Because a home that has been lived in fully carries something no neutral palette can replicate. It has presence. It has coherence. It has conviction. Buyers do not respond to emptiness. They respond to authenticity.

Endless expanses of neutrals might offend no one, but they inspire no one either. They exist in a kind of suspended neutrality, waiting for permission to become something else.

A decorated home, one that has been lived in and cared for, offers evidence of permanence. It shows that the structure was worthy of investment, it was worthy not only financially, but emotionally. It shows that someone trusted the home enough to inhabit it fully. That trust has value.

A home must feel permanent and anchored. It should not feel disposable. It should neither be assembled from materials designed for replacement, nor lived in cautiously for the sake of resale. It should be inhabited fully, honestly, and without apology.

Raising children on ‘nice’ furniture and flooring helps them know that they are trusted and valued. Pets can be trained to respect property. Do not relinquish your life and time to “children and pets” at the expense of quality and permanence. Even if an item sustains damage, that damage carries a history of time and place. It will bring wistful memories when there is peace and order in the house.

I encourage my clients to buy the nice furniture while their children are young. Let them inhabit a home, not just a ‘playhouse.’ Help them understand value, boundaries. Help them learn care and consideration. That is a priceless education.

Choose what you love and it will endure.

Live where you are.

When the time comes, the market will recognize the difference.

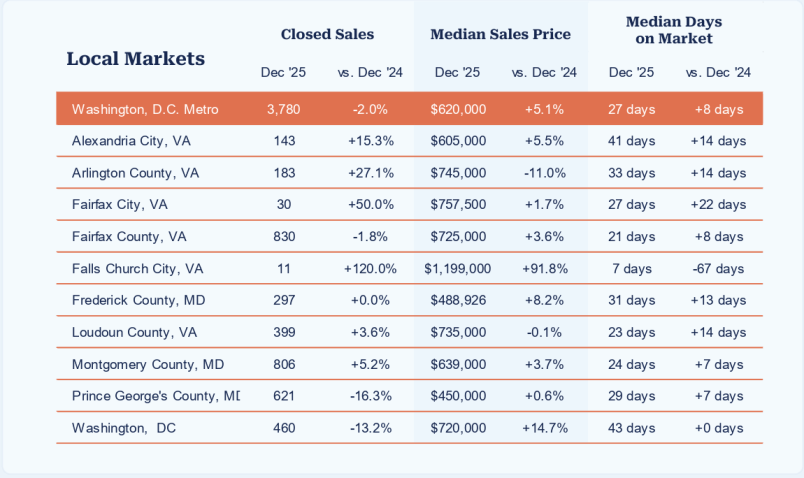

The December data from BrightMLS offers a reassuring close to the year across most of the Washington Metro region. Activity remains steady, prices appear to be resilient, and while days on market have stretched modestly, conditions continue to favor well-prepared buyers and sellers.

Northern Virginia and suburban Maryland performed particularly well. Alexandria, Arlington, Fairfax, Falls Church City, Loudoun, Montgomery, and Frederick Counties all showed solid to improving sales activity with generally stable or rising median prices. The increase in days on market across these areas reflects normalization rather than weakness. Buyers are deliberate, inspections matter, and pricing discipline is rewarded.

While median prices in D.C. rose year-over-year, closed sales declined and days on market remained elevated. This divergence is largely driven by the condominium sector, where rising condo fees, insurance costs, and buyer sensitivity to monthly carrying expenses continue to suppress demand. Well-located single-family homes and townhomes remain competitive.

This is not a distressed market at all. It is a discerning one and the panic to buy ‘something’ seems to have passed.

Homes that are priced correctly, are well-presented, and are aligned with buyer expectations are selling well. Those that are not, are waiting. Now, strategy, preparation, and thoughtful positioning matter more than ever.

Real estate decisions should always be made locally, not generically. The data reinforces what we, at Properties on the Potomac, Inc. see daily. Sales are driven by activity and not by headlines.

Do you have a low mortgage that you hate to give up? But you want a different living environment? Krasi Henkel has a plan for you. One that builds equity, wealth, and curates your lifestyle. Text Krasi – 703-624-8333

After attending the Loudoun County Chamber of Commerce ‘PolicyMaker Series: Postelection Aftermath’ I walked away with concerns and considerations. This blog is not intended to make or take a political stand, but to outline possibilities and current actions. Keeping you informed so that you can make the best possible decisions, is always my goal.

Politicians and analysts banter the term, affordable housing. Let’s unpack this concept and discover how, if at all, affordability can be affected.

The variables of affordability consist of the following obvious pieces:

The price of real estate

The mortgage interest rate

The mortgage term (number of years)

Cost to insure

Taxes

Income tax incentives (if any)

Housing supply and local zoning

To improve affordability, one or more of the above variables must be influenced as follows:

Private property values are subject to market forces.

Mortgage interest rates while variable, can be subsidized by jurisdictions or offset by tax savings

The term of the mortgage 15-30-50 affects the monthly payment

Insurance is partly environmental risk based, and partly determined by your desired value to insure and what to include.

Taxes – real estate taxes are based on jurisdictional assessments. You can appeal assessments. You can elect officials who would reduce tax rates.

The Federal government or even the state can make interest, taxes, etc. deductible at higher rates – AKA – subsidizing through deductibility.

Supply and demand shifts from scarcity to accessibility can partially be accomplished through thoughtful zoning and maybe expeditious reviews.

Below are possible solutions but will require bold federal and state participation.

Let’s clear one thing up – homeowners do not plan to decrease the asking prices for their houses in a scarcity scenario. Insurers have suffered massive losses and will likely not be reducing their rates, and their reinsurers will most likely not be doing the same.

Property taxes – you can evaluate your jurisdictional budgets and determine potential austerity measures with which to justify tax reductions. We all know that this is a long term project involving studies, hearings, and elections.

While on the topic of property taxes and local jurisdictions, one way to increase supply would be to loosen zoning regulations and shorten permit and inspection periods. All of that requires public hearings. Realistically, when was the last time a voting block voted to increase density?

Income tax deductibility or credits could be useful subject to income limits. This will require political maneuvering, bills, vetoes, and committees, and lots of talk and perhaps a little help.

Mortgage interest is a possible variant. When affordability is addressed, it is often addressed for first time home buyers. The US government, states, and local governments offer mortgage loans to offset cash down payments, and structure loans based on a variety of criteria. This is where creativity can set in and offers interesting options to consider.

Let’s look at Virginia for example. There are several assistance loan products including down payment and closing cost grants. After that there is Virginia Housing (formerly VHDA), which is funded through bonds and are not and do not affect the tax base. These loans come with quite a few strings and qualification can be onerous. Looking at today’s mortgage rate, I note that VHDA is offering their loan for 6.5%. Yet FHA, VA, USDA are all below 6%.

Another mortgage alternative is increasing the loan amortization terms from 30 to 50 years. Yes, the total interest paid will be higher, but the monthly payment can become affordable. Consider the example below:

$500,000 loan at 5.75%

30 year principal and interest (PI) payment: $2918

50 year principal and interest (PI) payment: $2540

The monthly savings will be: $ 378

That difference can make the difference in qualifying.

It will cost more over the life of the loan. The reality is that most people move every seven years. Loans can be refinanced if rates decline. I have met very few people who retained their original loan to its final payment. The 30-year mortgage was originally tied to the 30-year treasury bill. Though, the 10-year Treasury Note is a more direct benchmark. The 30-year treasuries are called “long bonds.”

Zoning:

Zoning adjustment measure has been on Virginia’s local jurisdiction radar for over five years. Since 2020 initiatives to modify local zoning to permit density increases have been proposed.

Last week, a circuit court judge recently ruled in favor of the City of Alexandria in the “Zoning for Housing” lawsuit, dismissing the case and allowing the city’s zoning reforms to stand.

The case had been brought by local property owners, Coalition for a Livable Alexandria, protesting the density changes and their perceived impact on their properties. This ruling allows the city’s “Zoning for Housing” ordinance to proceed.

A question: with the decision in place, can a developer now buy a single family house, tear it down and build a multi-family structure? What are the limits? What are the safeguards? Where will those residents park? How will the existing infrastructure support the additional density as far as education and traffic?

In Tysons, a similar initiative has been enacted. Click here to learn more about these and other Virginia measures.

While political promises abound, reality sets in. The recent election platform was heavy on affordable housing. When I inquired at the recent event, about the “how” of the promises, the moderator ‘ran out of time.’ I asked why VHDA loan rates outstrip all other loan rates. When I approached one of the State senators, he told me that they are “looking into it.” The urgency? Subject to interpretation. They seem focused on zoning changes as the primary solution.

There is no easy fix. Everyone must get involved and ask the hard questions: When politicians promise ‘affordable housing,’ ask them: Affordable to BUY, or affordable to RENT? Those are two very different things – one builds wealth and independence, the other creates permanent tenants beholden to landlords and government programs. The days of happy ambivalence are gone. You should pay close attention and make your decisions thoughtfully.

If you want to buy your first home, contact Broker Krasi Henkel. Her nearly 40 years of experience and exceptional lender network, produce dream-come-true scenarios. If you want to be one of the lucky few – text Krasi today – 703-624-8333.

The kitchen remains the heartbeat of the home. In the DC Metro area, that heartbeat is growing stronger, richer, and infinitely more personal. From the brownstones of Capitol Hill to the farms of Loudoun County, homeowners are redefining what “modern” means. The sterile, all-white kitchens of a decade ago are quietly stepping aside. Warmth, craftsmanship, and individuality have taken center stage.

Let’s explore what is truly cooking for 2026.

1. Character Returns

Today’s kitchens tell a story. They are designed, not decorated. The most sought-after spaces now feature authentic materials and honest finishes—the kind that feel as good as they look.

Quartzite and porcelain countertops are surpassing basic granite. They resist heat, stains, and trends. Natural wood cabinetry in walnut or white oak restores warmth where stark white once ruled. Textured stone backsplashes and reclaimed timbers add soul.

Even sustainability has become elegant. Low-VOC finishes, reclaimed materials, and energy-efficient appliances now speak the language of quiet luxury.

Professional insight: When we prepare a property for sale, we highlight craftsmanship. Words like “handcrafted,” “solid wood,” and “natural stone” signal value and permanence that buyers instinctively trust.

2. No Fear Color

Color is returning with sophistication and restraint. In the DC market, sage greens, deep blues, and soft charcoals are leading the palette. Two-toned cabinetry adds depth without shouting. Matte-black and aged-brass fixtures deliver contrast and timeless polish.

These tones look beautiful in person—and even better in photographs. They lend dimension and warmth that resonate both online and during showings.

Professional insight: Use color intentionally. Pair one rich tone with quiet neutrals for balance. Buyers are responding to kitchens that feel lived-in yet refined.

3. The Age of the Invisible Appliance

Technology has matured. The smartest kitchens in 2026 will not show off. They simply perform.

Panel-ready refrigerators blend into cabinetry. Induction cooktops sit flush with stone counters. Faucets activate by voice. Motion lighting and concealed charging drawers simplify daily life.

The effect is calm and seamless. Luxury is now defined by what is not seen.

Professional insight: When describing a property, mention “panel-ready,” “integrated,” or “concealed.” These terms suggest craftsmanship and elevate perception before a buyer ever steps inside.

4. Quiet Luxury Meets Modern Organic

The new aesthetic is calm confidence. Imagine soft textures, composite stone or porcelain, and handcrafted wood. Lighting is layered and warm. Metals are brushed, not polished. Nothing competes for attention, yet everything matters.

It is a blend of elegance and ease—modern design softened by organic detail.

Professional insight: Replace sterile with soulful. A matte brass fixture or walnut island base can change how a space feels. Buyers sense authenticity immediately.

5. Kitchens That Work as Hard as We Do

Life has changed. Our kitchens have adapted. Islands are no longer just for prep—they are command centers. Mornings start with coffee; afternoons bring laptops; evenings, charcuterie.

Storage solutions are smarter, and every inch is purposeful. The modern kitchen supports living, not just cooking.

Professional insight: When staging, create lifestyle moments. A laptop and mug says “home office.” A board of fruit and cheese says “gathering.” Buyers see themselves in that story.

Summary

The most desirable kitchens in the DC Metro area share the qualities of warmth, intelligence, and individuality. They are personal, practical, and timeless.

Whether your goal is to remodel, sell, or simply be inspired, remember: the perfect kitchen does not chase trends. It quietly defines them.

Contact Broker Krasi Henkel for referrals of kitchen experts or to discuss your next home. Best to text 703-624-8333

There seems to be a growing trend toward “burning bridges” as a form of self-assertion. It appears often, even celebrated, as though torching a connection is a mark of independence or strength.

Let’s pause and ask, “why?” To satisfy an ego? To prove a point? To protect ourselves from discomfort?

The truth is simpler. We never know when a door might open again. By burning the bridge, we limit opportunity. By leaving it standing, even unused, we preserve possibility.

Years ago, I worked for an exceptionally brilliant executive director. At our staff meetings, he would always end with the same words: “Be nice. You never know who your next boss will be.”

That line has stayed with me for more than five decades. The wisdom is timeless. Being nice costs nothing, and it buys peace of mind, grace, and long memories in one’s favor.

When negotiating with a difficult client or agent, consider the value of restraint. Not every disagreement demands destruction. Some require distance, but distance is different from demolition.

Of course, there are rare situations that justify a clean break. Yet in my many decades of business—as an auditor, portfolio manager, director, Realtor®, and broker, I am grateful that I have resisted the temptation to light the match. The people who might have deserved the flame have long since forgotten, and those who would have cared might have turned away.

Fire is satisfying only for a moment. Bridges, however, can stand for a lifetime.

You check one website for your home’s value, your neighbor uses another, and a potential buyer pulls up their phone during a showing to see what the “computer” says. After 39 years in real estate, I can tell you this: automated valuations are just sophisticated guesswork—and relying on them can cost sellers thousands.

The Algorithm Problem: Automated Valuation Models analyze data points: square footage, recent sales, tax records, etc. But what is more important is what they cannot analyze: the custom kitchen renovation that transformed your home, the problematic drainage in that “comparable” sale, or the fact that the house down the street sold quickly because of a job relocation, not market value.

Technology can do a lot, but it is important to understand that it misses:

Unique property features that add or subtract value

Neighborhood nuances invisible to databases

Market timing and seller motivation

Property condition variations

Jurisdictional changes affecting value

Micro-market trends within broader areas

Technology handles data processing efficiently. Humans interpret what that data means for your specific situation. An experienced agent knows that the “comparable” sale had certain issues, understands how a new development affects traffic patterns, and recognizes when timing creates opportunity or urgency.

Smart real estate professionals use technology as a starting point, not the final answer. Digital tools help us research, market, and communicate more effectively. They cannot replace the judgment that comes from walking through properties, understanding client needs, and reading market conditions that change faster than algorithms can adapt.

Algorithms can also distort appraisals—and that is where a competent, experienced agent can set the record straight. Several years ago, we listed a substantial property purchased by a tech professional who handled everything online, from discovering the listing to applying for a mortgage to the appraisal. The appraisal came in far below the contract price. Why? The appraiser spent barely five minutes at the property and based his assessment almost entirely on lot size and square footage, missing the unique features that truly defined its value.

What the ‘appraiser’ missed was the level of finishes and upgrades, including the brand new kitchen with state-of-the-art appliances and finishes, the renovated bathrooms, the newly installed hickory hardwood floors, the luxurious landscaping and hardscape throughout the back yard, and the new roof. The value of the missed elements exceeded 4 times the appraisal shortfall.

That is when the listing agent shut down technology and insisted on a local lender with local appraisers. The cost to the buyer was less than their internet options. The appraiser who visited spent extensive time learning the features and benefits of the particular property and submitted an appraisal slightly over contract price. They spent over an hour at the property. So—five rushed minutes with a checklist versus a full hour recognizing the details that truly defined the property’s worth. Which do you think produced the more accurate value?

At Properties on the Potomac, Inc. we use technology and automation to complete tasks. We use intellect and experience to value our clients’ properties. In a market where precision matters, you need someone who combines technological efficiency with human insight—especially in our Potomac area where unique properties and varying market conditions require local expertise that no algorithm possesses.

When choosing a listing agent, experience and strong support should be at the top of your list—your home deserves nothing less. To connect with one of our experienced agents, call or text 703-624-8333 today!

As cherry blossoms grace our beautiful capital, the DC Metro real estate market is experiencing subtle yet important shifts. At Properties on the Potomac, we’ve carefully analyzed current trends to provide you with a comprehensive outlook for the next six months, helping you navigate this evolving landscape with confidence.

Understanding the Market Adjustment

The Washington DC Metro area has always demonstrated remarkable resilience during economic fluctuations, largely due to our unique relationship with the federal government. Recent developments in the stock market, trade policies, and federal workforce adjustments are now creating noticeable ripples across our real estate landscape.

Rest assured—this is not a repeat of 2008. What we’re experiencing is a market recalibration rather than a crash. Most property segments will see modest corrections rather than steep declines, with transaction volume likely decreasing by 10-15% compared to previous years.

Federal Employment Impact

Recent federal workforce adjustments have introduced some uncertainty into our market. However, historically, DC’s government employment tends to stabilize more quickly than private sector jobs during economic shifts.

What’s particularly notable is the neighborhood-specific impact we’re observing. Areas closely tied to certain agencies may experience localized effects, while contractors and supporting businesses might face more significant adjustments than direct federal employees.

Interest Rate Outlook

For prospective buyers hoping for interest rate relief, we recommend maintaining realistic expectations. The Federal Reserve appears committed to its current positions given ongoing inflation concerns, suggesting mortgage rates will likely remain at current levels throughout 2025.

This interest rate environment continues to limit refinancing opportunities while presenting challenges for first-time buyers. Rather than waiting for potential rate drops, we encourage clients to focus on finding value in today’s market conditions.

Inventory Considerations

Despite economic headwinds, housing inventory levels remain historically low throughout the region. New construction continues to face supply chain and labor challenges, though we anticipate a modest inventory increase as some federal workforce shifts occur.

This slight inventory expansion won’t be sufficient to create a strong buyer’s market, but it does present negotiation opportunities that were simply unavailable during the competitive pandemic market.

Market Segment Analysis

Luxury Properties ($1M+) This segment faces the strongest headwinds, with 5-8% price adjustments expected. Properties remaining on the market for 60+ days are becoming more common. However, this creates a genuine opportunity window for financially secure buyers who have been waiting for more leverage.

Mid-Market Properties ($600K-$1M) This segment demonstrates remarkable resilience. Expect price stability with only minor adjustments (1-3%). Properties in premium locations maintain their value better than those in peripheral areas, reinforcing the timeless principle that location remains paramount during uncertain periods.

Entry-Level Homes (Under $600K) Strong demand persists in this segment, though affordability challenges are increasingly evident. While competitive bidding has cooled, well-priced properties continue to move quickly. We’re also noting renewed investor interest as rental demand remains robust throughout the region.

Geographic Insights

District of Columbia Historic neighborhoods like Georgetown and Capitol Hill continue showing remarkable stability, while emerging areas demonstrate greater price sensitivity. The condominium market is adjusting more quickly than single-family homes, potentially creating opportunities for long-term investors.

Maryland Suburbs Montgomery County maintains its reputation for stability, while Prince George’s County attracts increased interest driven by relative affordability. Areas with convenient public transit consistently outperform car-dependent neighborhoods.

Northern Virginia The ongoing Amazon HQ2 effect provides a welcome balance to federal contractions. Arlington and Alexandria maintain strong market positions, while technology corridor growth continues attracting professionals despite broader economic uncertainty.

Strategic Recommendations

For Sellers – Price realistically based on current conditions, not past market peaks – Invest in proper preparation and staging—presentation is increasingly important – Prepare for potentially longer marketing periods – Consider timing relative to federal policy announcements

For Buyers – Recognize the emerging window for negotiation leverage – Focus on long-term neighborhood fundamentals rather than short-term discounts – Secure financing pre-approvals early in your search process – Consider properties with “good bones” that may need updates

For Investors – The rental market remains strong as home purchasing power adjusts – Focus on properties near stable employment centers – Be selective with renovation projects given ongoing supply chain considerations – Plan for longer-term investments (5+ years) for optimal returns

Our Perspective The Washington DC Metro real estate market is experiencing an adjustment period rather than a crisis. Our region’s fundamental economic strengths remain intact despite short-term challenges. The coming months will reward strategic buyers and sellers who understand neighborhood-specific dynamics and maintain a long-term perspective.

Have questions about how these trends might affect your specific property or search? Contact Properties on the Potomac at 703-624-8333for a personalized consultation tailored to your unique situation.

Navigating Uncertainty: Real Estate at a Crossroads Never has the real estate landscape been so contradictory – simultaneously showing signs of strength and vulnerability. Are we facing a boom, a bubble, or an impending bust?

Properties on the Potomac’sKrasi Henkel has accurately predicted the last three real estate cycles from downturns to upswings. Her proven foresight is more valuable than ever in today’s complex market.

While technology floods us with information at unprecedented speeds, we mustn’t forget the human element of real estate – these are decisions about your most significant asset and potentially your largest liability.

Are We Heading for Another 2008? The question on everyone’s mind: Are we reliving 2007, with 2026 poised to mirror the 2008 collapse? Perhaps – but today’s landscape features critical differences:

Severe Housing Shortage: Virginia alone faces a deficit of 300,000-500,000 units

Historic Low Affordability: Homeownership remains out of reach for many

Improved Interest Rates: Creating new opportunities for strategic buyers

Record-High Prices: Pushing market elasticity to its limits

Building Market Pressure: Indicators point toward an inevitable correction

Make Decisions with Expertise, Not Algorithms Should you buy now? Is it time to sell? These questions demand more than automated valuation models and trending hashtags.

With firsthand experience navigating multiple real estate cycles, Krasi has developed a proprietary system to help Properties on the Potomac clients evaluate their options and craft intelligent, personalized strategies.

The bottom line: Don’t trust algorithms alone with your financial future. At Properties on the Potomac, Inc., our agents bring sophisticated understanding of real estate economics, finance, and equity evaluation to every client relationship.

Our singular mission is protecting our clients’ best interests during these uncertain times. For 2025, we have limited availability to welcome new clients. Don’t miss your window to explore your options with true market experts.

The rise of iBuyer or “instant cash offer” programs has introduced a new way for homeowners to sell their properties quickly. These companies, backed by deep-pocketed investors, purchase homes directly from sellers, often closing transactions in just days. Unlike traditional homebuyers looking for a place to live or rent out, iBuyers aim to buy at the lowest possible price, make necessary repairs, and quickly resell the home for a profit. While this model provides convenience, sellers should fully understand the pros and cons before deciding if this is the best option for them.

Advantages for Sellers

No need to make repairs before selling

Flexible options to cater to urgent selling timelines

Guidance from local real estate experts

A streamlined, turnkey process covering:

Contracts

Disclosures

State laws

Negotiations

Disadvantages for Sellers

Instant home purchase offers prioritize the iBuyer’s profit, not the seller’s best interest

Sellers typically receive low offers and still pay high fees, sometimes exceeding traditional agent commissions

The True Costs of iBuying iBuyer platforms operate with the goal of making a profit. That means the offers they make are often significantly lower than market value. On top of that, sellers face additional fees. While iBuyers market themselves as a way to avoid agent commissions, the reality is that their convenience fees range from 6% to 9.5%. Some even charge sellers additional fees that buyers would typically cover, adding another 1% or more to the cost.

In total, the direct costs of selling to an iBuyer—excluding repair credits—can range from 7% to 10%, compared to the 5% to 9% in total costs when selling through a traditional agent. That “convenience” often results in sellers giving up a significant portion of their hard-earned equity.

Repairs and closing costs are another key issue. In a traditional sale, these expenses are negotiable. With an iBuyer, there is no room for negotiation—sellers are simply charged for any necessary repairs. Once the iBuyer acquires the property, they will list it on the market, often for a higher price, within weeks.

Why Using an Agent May Be the Better Choice The primary goal of iBuyers is to make money—not to give sellers the best deal. However, homeowners looking for a fast and hassle-free sale can still achieve that with an experienced real estate agent. Rather than eliminating agents from the process, the key to a smooth and profitable sale is proper preparation and an aggressive pricing strategy.

Before accepting an iBuyer’s offer, consult a knowledgeable real estate professional. Invite an agent to review your net offer from the iBuyer before signing anything. A thorough analysis can reveal just how much equity you might be giving up. If an iBuyer sees your home as a profitable investment, you should take a closer look at your options before handing over your property at a discount.

We break down the numbers in the video below:

Check out this real-world example of a home sale completed with a realtor versus an iBuyer.

As shown in the video, that’s over 10% less than what you could earn from a traditional sale. Is the convenience really worth that much? Your home is likely your largest asset—don’t let an iBuyer take a big cut of your investment.

For more details, check out this article from Realtor.com.

Final Thoughts If you’re considering selling to an iBuyer, take the time to explore all your options. Before signing anything, consult with a real estate professional who can give you a clear picture of your home’s true value and the potential costs involved. You worked hard for your home—make sure you’re making the best financial decision for your future.

If you’re in the DC Metro area, give Properties on the Potomac a call at 703-624-8333 today!

Your mortgage lender required homeowners insurance, so you’re fully protected, right?

Think again.

The insurance industry operates through a complex network of insurers and reinsurers. When you purchase a policy from companies like State Farm, Travelers, or Erie, they transfer portions of their risk to other companies, often international firms. This process mirrors how your mortgage may be sold to a third party shortly after closing.

Recent catastrophic events have exposed cracks in this system. The cascade of disasters – hurricanes devastating the Southeast, the 2023 Lahaina wildfires in Maui, and the Palisades fires in Los Angeles – has overwhelmed insurance companies. Thousands of homeowners are now stuck in limbo, waiting months or even years for rebuilding funds as insurers struggle with depleted reserves and unresponsive reinsurers.

Don’t wait for disaster to strike. Take these critical steps now:

1. Contact your insurance company to understand their exact claims process and timeline 2. Request information about their reinsurance partnerships and those companies’ track records 3. Obtain a complete copy of your policy – not just the Declarations page 4. Review all coverage limits, exceptions, and exclusions in detail 5. Monitor your mail vigilantly for policy changes or non-renewal notices

A disturbing trend has emerged: in both Lahaina and Los Angeles, insurance companies sent non-renewal notifications to many homeowners shortly before disaster struck. Missing these notices could leave you completely unprotected.

While legislators debate reforms around reinsurance and claims processes, you must protect yourself now. Know your coverage, understand the claims process, and assert your rights as a policyholder. Your financial security depends on it.

Remember: The time to review your insurance coverage is before you need it. Make that call today.

Thinking about buying a home and want more tips for handling insurance? Contact Properties on the Potomac at 703-624-8333 today!