Many people design their homes with a future buyer in mind. They choose neutrals whether or not they like them. Yes, it is safe. It might not offend anyone. They live cautiously, as if tenants in their own homes.

As a first-time homebuyer, I made different decisions. I chose to decorate our home. I did not ‘stage’ it. I did not neutralize it. I decorated it to our taste and expectations. It was not expensive, simply lovely.

I was warned repeatedly. “Nobody will buy this when you want to sell.” ‘They’ were wrong. Not only did my homes sell, they sold quickly and for top values. Even when two of my two-story foyer walls were enameled in hunter green.

Why? Because a home that has been lived in fully carries something no neutral palette can replicate. It has presence. It has coherence. It has conviction. Buyers do not respond to emptiness. They respond to authenticity.

Endless expanses of neutrals might offend no one, but they inspire no one either. They exist in a kind of suspended neutrality, waiting for permission to become something else.

A decorated home, one that has been lived in and cared for, offers evidence of permanence. It shows that the structure was worthy of investment, it was worthy not only financially, but emotionally. It shows that someone trusted the home enough to inhabit it fully. That trust has value.

A home must feel permanent and anchored. It should not feel disposable. It should neither be assembled from materials designed for replacement, nor lived in cautiously for the sake of resale. It should be inhabited fully, honestly, and without apology.

Raising children on ‘nice’ furniture and flooring helps them know that they are trusted and valued. Pets can be trained to respect property. Do not relinquish your life and time to “children and pets” at the expense of quality and permanence. Even if an item sustains damage, that damage carries a history of time and place. It will bring wistful memories when there is peace and order in the house.

I encourage my clients to buy the nice furniture while their children are young. Let them inhabit a home, not just a ‘playhouse.’ Help them understand value, boundaries. Help them learn care and consideration. That is a priceless education.

Choose what you love and it will endure.

Live where you are.

When the time comes, the market will recognize the difference.

Rentals. Their management and tenancy are a significant part of real estate ownership. At Properties on the Potomac, we follow legislative updates in all three of our jurisdictions: Virginia, Maryland, and Washington, D.C. Each has its own landlord-tenant laws that must be carefully observed.

As professionals, we help property owners secure good tenants who care for their homes. We do this across all three jurisdictions. We also assist past clients who are transitioning into rentals for lifestyle changes or interim situations.

Unlike residential sales, rentals are governed largely by statute. Landlord-tenant laws affect day-to-day operations, which can significantly impact a landlord’s finances.

Affordable housing is a major topic today. Alongside that discussion, tenant rights and landlord obligations are receiving increased attention. Maryland has already enacted stricter rules involving security and pet deposits. Virginia is considering several similar measures.

Security Deposit rules by jurisdiction

(their refund rules will be addressed in a future blog):

Washington, D.C. All security deposits must be held in FDIC-insured escrow accounts and must accrue interest.

Maryland Security deposits are limited to one month’s rent. Pet deposits are not allowed, though landlords may negotiate non-refundable rent increases related to pets. All deposits must be held in FDIC-insured escrow accounts.

Virginia There is currently no cap on security deposits, and no escrow or interest requirement. However, this may change with pending legislation.

Delinquent Rents and Eviction Initiation

Washington, D.C. Landlords must provide 30 days written notice of nonpayment. Tenants may cure during that period.

Maryland Tenants generally have 10 days to pay or vacate. The eviction process itself is often lengthy.

Virginia Currently requires a 5-day pay-or-quit notice. Proposed legislation would extend this to 14 days.

It is critical that landlords follow the rules of their jurisdiction. Failure to comply can result in loss of deposits, unnecessary repair responsibilities, fines, and delayed legal action.

For many landlords, working with a professional property manager helps reduce risk and keeps operations compliant.

Virginia Legislative Updates – 2026 Session

When I attended the Northern Virginia Association of Realtors Legislative Day in Richmond on January 29, I learned about several landlord-tenant bills currently under consideration in the Virginia General Assembly. Many could meaningfully affect landlords.

Eviction and Payment Reforms

• HB 15 (Price) — Extends the grace period for late rent payments from 5 days to 14 days before eviction proceedings may begin. • HB 95 (Bennett-Parker) — Requires landlords to offer payment plans of up to six months to tenants behind on rent before terminating a lease. • HB 281 (Callsen) / SB 373 (Boysko) — Removes the requirement for tenants to pay disputed rent into court before asserting legal defenses. • HB 837 (McClure) / SB 273 (Locke) — Updates the Eviction Diversion Program’s eligibility and notification process.

Fees and Maintenance

• SB 313 (Ebbin) / HB 1005 (Price) — Prohibits landlords from charging for routine maintenance unless caused by a tenant’s lease violation. • HB 1409 (Schmidt) — Bans certain charges for common-area utilities, delivery fees, and services beyond actual costs. • SB 349 (Locke) — Limits pre-tenancy fees and requires full written disclosure prior to showings.

Tenant Protections

• HB 14 (Price) — Allows local governments to pursue legal action against landlords who fail to correct hazardous conditions. • HB 1408 (Schmidt) — Expands protections for victims of family abuse. • HB 1252 (McClure) — Requires disclosure of algorithmic rent-pricing tools and allows tenants to request human review. • HB 329 (McClure) — Expands definitions of retaliatory conduct and tenant remedies.

Local Authority and Market Regulation

• HB 278 (Clark) — Allows local governments to adopt anti-rent gouging policies. • SB 547 (Sturtevant) — Limits ownership of single-family homes by certain entities and requires public marketing periods.

As a current or prospective landlord, review these proposals and determine how they might affect your properties and investments. You have the right to address concerns or express support with your elected representative.

At Properties on the Potomac, we track legislative changes closely to help our clients stay informed and prepared.

If you own rental property and have questions, we are available to help. Text Broker, Krasi Henkel to discuss your questions.

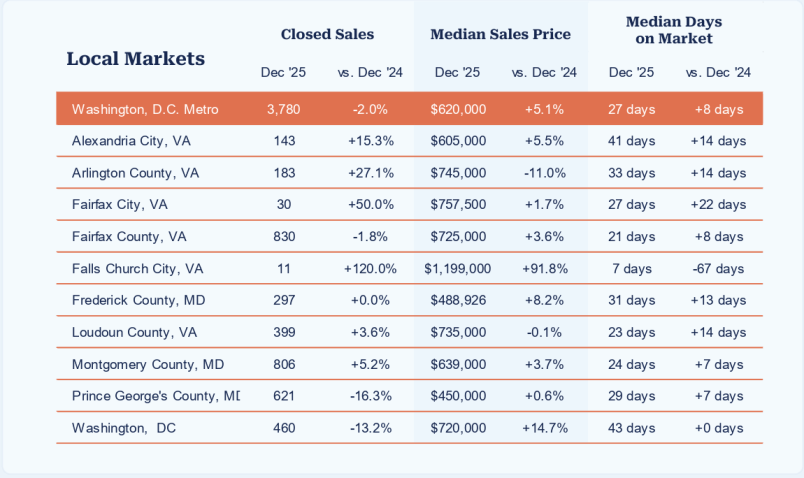

The December data from BrightMLS offers a reassuring close to the year across most of the Washington Metro region. Activity remains steady, prices appear to be resilient, and while days on market have stretched modestly, conditions continue to favor well-prepared buyers and sellers.

Northern Virginia and suburban Maryland performed particularly well. Alexandria, Arlington, Fairfax, Falls Church City, Loudoun, Montgomery, and Frederick Counties all showed solid to improving sales activity with generally stable or rising median prices. The increase in days on market across these areas reflects normalization rather than weakness. Buyers are deliberate, inspections matter, and pricing discipline is rewarded.

While median prices in D.C. rose year-over-year, closed sales declined and days on market remained elevated. This divergence is largely driven by the condominium sector, where rising condo fees, insurance costs, and buyer sensitivity to monthly carrying expenses continue to suppress demand. Well-located single-family homes and townhomes remain competitive.

This is not a distressed market at all. It is a discerning one and the panic to buy ‘something’ seems to have passed.

Homes that are priced correctly, are well-presented, and are aligned with buyer expectations are selling well. Those that are not, are waiting. Now, strategy, preparation, and thoughtful positioning matter more than ever.

Real estate decisions should always be made locally, not generically. The data reinforces what we, at Properties on the Potomac, Inc. see daily. Sales are driven by activity and not by headlines.

Do you have a low mortgage that you hate to give up? But you want a different living environment? Krasi Henkel has a plan for you. One that builds equity, wealth, and curates your lifestyle. Text Krasi – 703-624-8333

It is the Holiday Season again. Social calendars and children’s activities are at their peak. A common belief is that December is “quiet” in real estate. In reality, things are abuzz preparing for the New Year. Realtors are planning and wrapping up their year. Many homeowners are thinking, while perhaps, not taking immediate action.

When the calendar slows, distractions abound. Plans percolate. There might be fewer sales. There is also less competition (good for buyers). Are you evaluating how your space functions? Conversations often shift from “Should we?” to “What do we want next?” What do you really want?

The Conversations That Matter Most

Planning conversations revolve around timing, readiness, and sequencing. Much depends on selling or holding the current property. Should you consider a more immediate or deferred approach?

What matters to you most? Do you need more space, a different location, more land? What does your next chapter look like?

Here is why early planning matters. Several years ago, a client shared some plans for the following year. We discussed options and made a plan. I received a distress call shortly before their listing was going on the market. A neighbor was also going on the market at the same time. “What should we do?” I assured them that we are ready to put the house on the market immediately. There were no properties for sale in the entire community. So, “Let’s get you several offers, the best buyer, and the best offer, and those who miss your house can have the next one.” This is exactly what happened. Soon after their sale, three more houses came on the market. There were no multiple offers. Our price remained top for the neighborhood for quite some time.

Financial Considerations

The financial and strategic conversations are inescapable – the “yes…but.” Yet, where there is a will there is a way. You most likely have equity in your current property which will benefit your future purchase. As a seller, tax advantages could help you act sooner than later. Perhaps now is a good time to have a preliminary conversation with your trusted real estate advisor.

Your three percent loan is marvelous, but you can still up or downsize despite interest rate fluctuations. I have structured many happy outcomes and helped my clients build wealth.

Waiting until January or worse, “spring” limits your options. January brings speed, competition, and many external pressures. Making reactive decisions is rarely optimal. Early conversations allow for better evaluation, preparation, and ultimately, execution.

As in any important financial consideration, thoughtful outcomes begin with thoughtful conversations. If you are considering a potential change, contact me now. I will help you sort the pieces and give you meaningful information with which to make good decisions. After all, the best real estate decisions are rarely rushed. They are considered.

This is the season when we spend more time indoors and our doors and windows remain closed for longer periods.

I am deathly allergic and toxic to mold. A three second exposure can make me ill for weeks and even months. I often laugh with my buyer clients that I am the official “mold meter” when we look at houses. There have been times that I detected mold even before opening the front door. I share my experience with my clients, and we leave as quickly as possible. Sick houses can be cleaned. My clients need not be the ones to do that.

Not everyone smells or reacts to mold. I believe that educating my clients is paramount. No sale is worth illness and maladies. I would rather walk away than knowingly let my clients buy into malaise, illness, and even life-threatening accidents. A mold reaction caused me to fall from my horse, breaking my ankle. My life changed. I have not been the same ever since.

While everyone has varying levels of reaction, if any, to mold in a property, it is important to understand how mold develops and where it can grow. It is not always the old basement, although it quite possibly can be. With weather changes and moisture changes, below is a list (not comprehensive but suggestive) where mold can grow:

Window casings and drywall around them

Doors – under sill plates and around the frames on the drywall

Under sink base cabinets

Under dishwashers

Under washing machines

Under HVAC condensate lines

Inside HVAC air handlers

Behind and under refrigerators (even those without water sources)

Bathrooms

Basements – under floors, wall bases, even ceilings

Your car!!

What can you do to prevent mold from taking root in your home or car?

Inspect window caulking regularly – recaulk as needed

Check door sill plates – especially at decks and patios

Look under sinks – look for evidence of moisture – attack and remediate

Look under your dishwasher for evidence of water and mold signs

Look under and behind washing machines

Have your HVAC serviced and inspected semi-annually – ask your tech to look for evidence of leakage and mold

Pull your refrigerator out – inspect the floor

Run the exhaust fan in your bathrooms while showering to prevent condensation build-up

Confirm that bathroom exhaust fans are operating properly

Change the air filter in your car

Keep all HVAC filters clean

Here are a few unsettling facts that I recently discovered:

Drywall in its manufacturing process has imbedded mold spores

Mold loves drywall. That is why after a water incursion event, mold grows on drywall very quickly.

New home construction can “build-in” mold during the construction process by allowing materials to get wet.

Your car’s trunk gasket can be allowing water incursion and harboring mold

Your car’s air filter can get damaged by mice – their deposits can sprout mold

Your car’s AC can leak into your dash – mold can sprout

These lists are just a few of the mold issues that can develop over time or quickly.

Mold has been associated with chronic fatigue syndrome, headaches, upper respiratory ailments, even ‘colds’ could be reactions to mold. Do not be lulled into security by a ‘new house.’

Last year, I walked through our basement bedroom for a split second. That was long enough for me to get sick. It lasted through January. Where was the mold? Our basement bath exhaust fan had stopped exhausting but sounded to be running just fine. My husband likes the shower there. The moisture from the shower traveled to the far corner of the room, settled on the cold tile floor under a night table, and sprouted a quarter-sized spot of mold.

As a precaution – I had the exterior walls’ drywall removed – luckily – all was dry including studs and base framing. The tile was dry with no evidence of water. I called a waterproofing company – they tried to sell me a $50,000 remediation system.

I decided to call on the home inspector who inspects my clients’ home purchases. He came armed with a moisture meter. He found none. Then, he suggested laying down and sealing a vapor barrier plastic sheet like that of a crawl space. He told us to leave it down for 7-10 days. If at the end of the period, there was moisture under the barrier – there is a water problem. If none, then it was a condensation problem. Luckily, it was the latter.

Our brilliant contractor figured out that the exhaust fan was not extracting the condensation. In with a new fan and lots of cleaning – all is well.

However, this episode required that I discard the entire contents of the room. I had my brand new furnace thoroughly cleaned and disinfected. Mold spores are airborne and had certainly settled on all fabrics and furnishings. All because an exhaust fan had malfunctioned. On that note – ask questions about the history of any resale furnishings that you are considering buying. Have you ever smelled mustiness in antique drawers . . . ?

Mold is toxic and for those who are sensitive, each episode increases that sensitivity and the reactions. While I am not a mold expert, here is a link to mold and its remediation on YouTube. The mold conversation begins around the 3 minute mark. It is a little long but could save you years of misery.

If you have questions or need resources, contact Krasi Henkel – TEXT – 703-624-8333. If you are planning to buy your next home, Text Krasi.

After attending the Loudoun County Chamber of Commerce ‘PolicyMaker Series: Postelection Aftermath’ I walked away with concerns and considerations. This blog is not intended to make or take a political stand, but to outline possibilities and current actions. Keeping you informed so that you can make the best possible decisions, is always my goal.

Politicians and analysts banter the term, affordable housing. Let’s unpack this concept and discover how, if at all, affordability can be affected.

The variables of affordability consist of the following obvious pieces:

The price of real estate

The mortgage interest rate

The mortgage term (number of years)

Cost to insure

Taxes

Income tax incentives (if any)

Housing supply and local zoning

To improve affordability, one or more of the above variables must be influenced as follows:

Private property values are subject to market forces.

Mortgage interest rates while variable, can be subsidized by jurisdictions or offset by tax savings

The term of the mortgage 15-30-50 affects the monthly payment

Insurance is partly environmental risk based, and partly determined by your desired value to insure and what to include.

Taxes – real estate taxes are based on jurisdictional assessments. You can appeal assessments. You can elect officials who would reduce tax rates.

The Federal government or even the state can make interest, taxes, etc. deductible at higher rates – AKA – subsidizing through deductibility.

Supply and demand shifts from scarcity to accessibility can partially be accomplished through thoughtful zoning and maybe expeditious reviews.

Below are possible solutions but will require bold federal and state participation.

Let’s clear one thing up – homeowners do not plan to decrease the asking prices for their houses in a scarcity scenario. Insurers have suffered massive losses and will likely not be reducing their rates, and their reinsurers will most likely not be doing the same.

Property taxes – you can evaluate your jurisdictional budgets and determine potential austerity measures with which to justify tax reductions. We all know that this is a long term project involving studies, hearings, and elections.

While on the topic of property taxes and local jurisdictions, one way to increase supply would be to loosen zoning regulations and shorten permit and inspection periods. All of that requires public hearings. Realistically, when was the last time a voting block voted to increase density?

Income tax deductibility or credits could be useful subject to income limits. This will require political maneuvering, bills, vetoes, and committees, and lots of talk and perhaps a little help.

Mortgage interest is a possible variant. When affordability is addressed, it is often addressed for first time home buyers. The US government, states, and local governments offer mortgage loans to offset cash down payments, and structure loans based on a variety of criteria. This is where creativity can set in and offers interesting options to consider.

Let’s look at Virginia for example. There are several assistance loan products including down payment and closing cost grants. After that there is Virginia Housing (formerly VHDA), which is funded through bonds and are not and do not affect the tax base. These loans come with quite a few strings and qualification can be onerous. Looking at today’s mortgage rate, I note that VHDA is offering their loan for 6.5%. Yet FHA, VA, USDA are all below 6%.

Another mortgage alternative is increasing the loan amortization terms from 30 to 50 years. Yes, the total interest paid will be higher, but the monthly payment can become affordable. Consider the example below:

$500,000 loan at 5.75%

30 year principal and interest (PI) payment: $2918

50 year principal and interest (PI) payment: $2540

The monthly savings will be: $ 378

That difference can make the difference in qualifying.

It will cost more over the life of the loan. The reality is that most people move every seven years. Loans can be refinanced if rates decline. I have met very few people who retained their original loan to its final payment. The 30-year mortgage was originally tied to the 30-year treasury bill. Though, the 10-year Treasury Note is a more direct benchmark. The 30-year treasuries are called “long bonds.”

Zoning:

Zoning adjustment measure has been on Virginia’s local jurisdiction radar for over five years. Since 2020 initiatives to modify local zoning to permit density increases have been proposed.

Last week, a circuit court judge recently ruled in favor of the City of Alexandria in the “Zoning for Housing” lawsuit, dismissing the case and allowing the city’s zoning reforms to stand.

The case had been brought by local property owners, Coalition for a Livable Alexandria, protesting the density changes and their perceived impact on their properties. This ruling allows the city’s “Zoning for Housing” ordinance to proceed.

A question: with the decision in place, can a developer now buy a single family house, tear it down and build a multi-family structure? What are the limits? What are the safeguards? Where will those residents park? How will the existing infrastructure support the additional density as far as education and traffic?

In Tysons, a similar initiative has been enacted. Click here to learn more about these and other Virginia measures.

While political promises abound, reality sets in. The recent election platform was heavy on affordable housing. When I inquired at the recent event, about the “how” of the promises, the moderator ‘ran out of time.’ I asked why VHDA loan rates outstrip all other loan rates. When I approached one of the State senators, he told me that they are “looking into it.” The urgency? Subject to interpretation. They seem focused on zoning changes as the primary solution.

There is no easy fix. Everyone must get involved and ask the hard questions: When politicians promise ‘affordable housing,’ ask them: Affordable to BUY, or affordable to RENT? Those are two very different things – one builds wealth and independence, the other creates permanent tenants beholden to landlords and government programs. The days of happy ambivalence are gone. You should pay close attention and make your decisions thoughtfully.

If you want to buy your first home, contact Broker Krasi Henkel. Her nearly 40 years of experience and exceptional lender network, produce dream-come-true scenarios. If you want to be one of the lucky few – text Krasi today – 703-624-8333.