It is the Holiday Season again. Social calendars and children’s activities are at their peak. A common belief is that December is “quiet” in real estate. In reality, things are abuzz preparing for the New Year. Realtors are planning and wrapping up their year. Many homeowners are thinking, while perhaps, not taking immediate action.

When the calendar slows, distractions abound. Plans percolate. There might be fewer sales. There is also less competition (good for buyers). Are you evaluating how your space functions? Conversations often shift from “Should we?” to “What do we want next?” What do you really want?

The Conversations That Matter Most

Planning conversations revolve around timing, readiness, and sequencing. Much depends on selling or holding the current property. Should you consider a more immediate or deferred approach?

What matters to you most? Do you need more space, a different location, more land? What does your next chapter look like?

Here is why early planning matters. Several years ago, a client shared some plans for the following year. We discussed options and made a plan. I received a distress call shortly before their listing was going on the market. A neighbor was also going on the market at the same time. “What should we do?” I assured them that we are ready to put the house on the market immediately. There were no properties for sale in the entire community. So, “Let’s get you several offers, the best buyer, and the best offer, and those who miss your house can have the next one.” This is exactly what happened. Soon after their sale, three more houses came on the market. There were no multiple offers. Our price remained top for the neighborhood for quite some time.

Financial Considerations

The financial and strategic conversations are inescapable – the “yes…but.” Yet, where there is a will there is a way. You most likely have equity in your current property which will benefit your future purchase. As a seller, tax advantages could help you act sooner than later. Perhaps now is a good time to have a preliminary conversation with your trusted real estate advisor.

Your three percent loan is marvelous, but you can still up or downsize despite interest rate fluctuations. I have structured many happy outcomes and helped my clients build wealth.

Waiting until January or worse, “spring” limits your options. January brings speed, competition, and many external pressures. Making reactive decisions is rarely optimal. Early conversations allow for better evaluation, preparation, and ultimately, execution.

As in any important financial consideration, thoughtful outcomes begin with thoughtful conversations. If you are considering a potential change, contact me now. I will help you sort the pieces and give you meaningful information with which to make good decisions. After all, the best real estate decisions are rarely rushed. They are considered.

After attending the Loudoun County Chamber of Commerce ‘PolicyMaker Series: Postelection Aftermath’ I walked away with concerns and considerations. This blog is not intended to make or take a political stand, but to outline possibilities and current actions. Keeping you informed so that you can make the best possible decisions, is always my goal.

Politicians and analysts banter the term, affordable housing. Let’s unpack this concept and discover how, if at all, affordability can be affected.

The variables of affordability consist of the following obvious pieces:

The price of real estate

The mortgage interest rate

The mortgage term (number of years)

Cost to insure

Taxes

Income tax incentives (if any)

Housing supply and local zoning

To improve affordability, one or more of the above variables must be influenced as follows:

Private property values are subject to market forces.

Mortgage interest rates while variable, can be subsidized by jurisdictions or offset by tax savings

The term of the mortgage 15-30-50 affects the monthly payment

Insurance is partly environmental risk based, and partly determined by your desired value to insure and what to include.

Taxes – real estate taxes are based on jurisdictional assessments. You can appeal assessments. You can elect officials who would reduce tax rates.

The Federal government or even the state can make interest, taxes, etc. deductible at higher rates – AKA – subsidizing through deductibility.

Supply and demand shifts from scarcity to accessibility can partially be accomplished through thoughtful zoning and maybe expeditious reviews.

Below are possible solutions but will require bold federal and state participation.

Let’s clear one thing up – homeowners do not plan to decrease the asking prices for their houses in a scarcity scenario. Insurers have suffered massive losses and will likely not be reducing their rates, and their reinsurers will most likely not be doing the same.

Property taxes – you can evaluate your jurisdictional budgets and determine potential austerity measures with which to justify tax reductions. We all know that this is a long term project involving studies, hearings, and elections.

While on the topic of property taxes and local jurisdictions, one way to increase supply would be to loosen zoning regulations and shorten permit and inspection periods. All of that requires public hearings. Realistically, when was the last time a voting block voted to increase density?

Income tax deductibility or credits could be useful subject to income limits. This will require political maneuvering, bills, vetoes, and committees, and lots of talk and perhaps a little help.

Mortgage interest is a possible variant. When affordability is addressed, it is often addressed for first time home buyers. The US government, states, and local governments offer mortgage loans to offset cash down payments, and structure loans based on a variety of criteria. This is where creativity can set in and offers interesting options to consider.

Let’s look at Virginia for example. There are several assistance loan products including down payment and closing cost grants. After that there is Virginia Housing (formerly VHDA), which is funded through bonds and are not and do not affect the tax base. These loans come with quite a few strings and qualification can be onerous. Looking at today’s mortgage rate, I note that VHDA is offering their loan for 6.5%. Yet FHA, VA, USDA are all below 6%.

Another mortgage alternative is increasing the loan amortization terms from 30 to 50 years. Yes, the total interest paid will be higher, but the monthly payment can become affordable. Consider the example below:

$500,000 loan at 5.75%

30 year principal and interest (PI) payment: $2918

50 year principal and interest (PI) payment: $2540

The monthly savings will be: $ 378

That difference can make the difference in qualifying.

It will cost more over the life of the loan. The reality is that most people move every seven years. Loans can be refinanced if rates decline. I have met very few people who retained their original loan to its final payment. The 30-year mortgage was originally tied to the 30-year treasury bill. Though, the 10-year Treasury Note is a more direct benchmark. The 30-year treasuries are called “long bonds.”

Zoning:

Zoning adjustment measure has been on Virginia’s local jurisdiction radar for over five years. Since 2020 initiatives to modify local zoning to permit density increases have been proposed.

Last week, a circuit court judge recently ruled in favor of the City of Alexandria in the “Zoning for Housing” lawsuit, dismissing the case and allowing the city’s zoning reforms to stand.

The case had been brought by local property owners, Coalition for a Livable Alexandria, protesting the density changes and their perceived impact on their properties. This ruling allows the city’s “Zoning for Housing” ordinance to proceed.

A question: with the decision in place, can a developer now buy a single family house, tear it down and build a multi-family structure? What are the limits? What are the safeguards? Where will those residents park? How will the existing infrastructure support the additional density as far as education and traffic?

In Tysons, a similar initiative has been enacted. Click here to learn more about these and other Virginia measures.

While political promises abound, reality sets in. The recent election platform was heavy on affordable housing. When I inquired at the recent event, about the “how” of the promises, the moderator ‘ran out of time.’ I asked why VHDA loan rates outstrip all other loan rates. When I approached one of the State senators, he told me that they are “looking into it.” The urgency? Subject to interpretation. They seem focused on zoning changes as the primary solution.

There is no easy fix. Everyone must get involved and ask the hard questions: When politicians promise ‘affordable housing,’ ask them: Affordable to BUY, or affordable to RENT? Those are two very different things – one builds wealth and independence, the other creates permanent tenants beholden to landlords and government programs. The days of happy ambivalence are gone. You should pay close attention and make your decisions thoughtfully.

If you want to buy your first home, contact Broker Krasi Henkel. Her nearly 40 years of experience and exceptional lender network, produce dream-come-true scenarios. If you want to be one of the lucky few – text Krasi today – 703-624-8333.

The rise of iBuyer or “instant cash offer” programs has introduced a new way for homeowners to sell their properties quickly. These companies, backed by deep-pocketed investors, purchase homes directly from sellers, often closing transactions in just days. Unlike traditional homebuyers looking for a place to live or rent out, iBuyers aim to buy at the lowest possible price, make necessary repairs, and quickly resell the home for a profit. While this model provides convenience, sellers should fully understand the pros and cons before deciding if this is the best option for them.

Advantages for Sellers

No need to make repairs before selling

Flexible options to cater to urgent selling timelines

Guidance from local real estate experts

A streamlined, turnkey process covering:

Contracts

Disclosures

State laws

Negotiations

Disadvantages for Sellers

Instant home purchase offers prioritize the iBuyer’s profit, not the seller’s best interest

Sellers typically receive low offers and still pay high fees, sometimes exceeding traditional agent commissions

The True Costs of iBuying iBuyer platforms operate with the goal of making a profit. That means the offers they make are often significantly lower than market value. On top of that, sellers face additional fees. While iBuyers market themselves as a way to avoid agent commissions, the reality is that their convenience fees range from 6% to 9.5%. Some even charge sellers additional fees that buyers would typically cover, adding another 1% or more to the cost.

In total, the direct costs of selling to an iBuyer—excluding repair credits—can range from 7% to 10%, compared to the 5% to 9% in total costs when selling through a traditional agent. That “convenience” often results in sellers giving up a significant portion of their hard-earned equity.

Repairs and closing costs are another key issue. In a traditional sale, these expenses are negotiable. With an iBuyer, there is no room for negotiation—sellers are simply charged for any necessary repairs. Once the iBuyer acquires the property, they will list it on the market, often for a higher price, within weeks.

Why Using an Agent May Be the Better Choice The primary goal of iBuyers is to make money—not to give sellers the best deal. However, homeowners looking for a fast and hassle-free sale can still achieve that with an experienced real estate agent. Rather than eliminating agents from the process, the key to a smooth and profitable sale is proper preparation and an aggressive pricing strategy.

Before accepting an iBuyer’s offer, consult a knowledgeable real estate professional. Invite an agent to review your net offer from the iBuyer before signing anything. A thorough analysis can reveal just how much equity you might be giving up. If an iBuyer sees your home as a profitable investment, you should take a closer look at your options before handing over your property at a discount.

We break down the numbers in the video below:

Check out this real-world example of a home sale completed with a realtor versus an iBuyer.

As shown in the video, that’s over 10% less than what you could earn from a traditional sale. Is the convenience really worth that much? Your home is likely your largest asset—don’t let an iBuyer take a big cut of your investment.

For more details, check out this article from Realtor.com.

Final Thoughts If you’re considering selling to an iBuyer, take the time to explore all your options. Before signing anything, consult with a real estate professional who can give you a clear picture of your home’s true value and the potential costs involved. You worked hard for your home—make sure you’re making the best financial decision for your future.

If you’re in the DC Metro area, give Properties on the Potomac a call at 703-624-8333 today!

If you recently received your property tax assessment and think it’s too high, you may have the option to appeal. Property tax assessments are used to determine how much you owe in taxes each year, and an inaccurate valuation could mean paying more than your fair share.

In the Washington, D.C., metro area, property owners in the District, Maryland, and Virginia each have different processes for appealing assessments. This guide will walk you through the basics of how assessments work, when you should consider an appeal, and the steps to challenge an incorrect valuation in D.C., Northern Virginia, and Maryland suburbs.

Understanding Your Property Tax Assessment Local governments assess property values based on market trends, recent sales of similar properties, and any improvements made to your home. This assessed value determines your annual property tax bill. However, assessments aren’t always accurate, and mistakes can happen, such as:

Failing to account for declining market conditions

If you believe your assessment is too high, an appeal may help lower your property taxes.

A professional appraisal can sometimes help an appeal.

General Steps to Appeal a Property Tax Assessment

Review Your Assessment Notice – Check for any discrepancies in your property details.

Research Comparable Properties – Find recent sales of similar homes in your area to support your case. Properties on the Potomac can assist with this.

Check for Errors – Ensure there are no mistakes in the assessment records.

File an Appeal by the Deadline – Each jurisdiction has specific deadlines and processes for appeals.

Present Evidence – Be prepared to provide documentation proving your property is over-assessed.

Now, let’s look at how the appeal process works in D.C., Northern Virginia, and Maryland suburbs.

Appealing Your Property Tax Assessment By Location: Click on the location to get additional details on how and where to file an appeal.

Washington, DC

Steps to Appeal:

Check Your Assessment – The Office of Tax and Revenue (OTR) mails annual assessments in late February or early March.

File a First-Level Appeal – You must submit your appeal to OTR by April 1 of the same year. The appeal can be filed online, by mail, or in person.

Attend a Hearing (If Necessary) – If your initial appeal is denied, you can request a second-level review with the Real Property Tax Appeals Commission (RPTAC).

Take Your Case to Court – If you’re still unsatisfied with the decision, you can file a case with the D.C. Superior Court.

Mail: Office of Tax and Revenue, 1101 4th Street, SW, Suite 550W, Washington, D.C. 20024

Northern Virginia: Arlington County, Fairfax County, Alexandria, Loudoun County, Prince William County

Steps to Appeal:

Review Your Notice – Assessment notices are typically sent in late February.

Request an Informal Review – Contact your local tax assessor’s office to discuss potential errors. This step is optional but may lead to a quick resolution.

File a Formal Appeal – Submit an appeal to the Board of Equalization (BOE) by varied deadlines (usually April-May, depending on the county).

Prepare for a Hearing – Provide sales data, appraisals, and other supporting evidence.

Maryland: Montgomery County, Prince George’s County, Frederick County

Steps to Appeal:

Review Your Assessment Notice – Maryland properties are reassessed every three years. Notices are sent out in late December for properties up for reassessment the following year.

Request a Reassessment (If Necessary) – If you believe your assessment is too high, you can file an appeal within 45 days of receiving your notice.

File an Appeal with the Supervisor of Assessments – If an informal review doesn’t resolve the issue, submit a formal appeal to the Property Tax Assessment Appeal Board (PTAAB).

Take Your Case to the Maryland Tax Court – If necessary, you can escalate your appeal beyond the PTAAB.

Meet Deadlines – Each jurisdiction has strict filing deadlines, so don’t miss your opportunity to appeal.

Use Comparable Sales Data – Provide recent sales of similar properties in your neighborhood to prove overvaluation.

Highlight Property Deficiencies – Document any structural issues, outdated systems, or factors that negatively affect your home’s value.

Get a Professional Appraisal – Hiring an independent appraiser can strengthen your case.

Final Thoughts A successful property tax appeal can save you money, but it requires research, preparation, and sometimes persistence. If you believe your home is over-assessed, following the steps outlined above for your specific jurisdiction can help you navigate the process.

If you’re looking for more guidance on property values or considering buying or selling in the D.C. metro area, our experienced team is here to help. Contact Tiffany Henkel at 703-989-7452 today!

When it comes to selling your home, the kitchen remains the heart of the house and often the deal-maker or breaker. But finding the perfect balance between impactful updates and smart spending can be tricky. Let’s explore how to maximize your kitchen’s appeal without overspending or under-improving.

Butcher block counters offer a more modern look without breaking the bank.You can often update cabinets by simply painting and adding new hardware.Under-cabinet lighting can instantly transform your kitchen with a more high-end look.

The Smart Money Zones The most impactful kitchen updates often focus on three key areas:

1. Countertops: Granite is no longer the automatic go-to. Consider these mid-range options that offer both beauty and value:

Quartz composites: Offer durability and style without the maintenance of natural stone

Butcher block: Add warmth and character at a reasonable price point

High-end laminate: Modern options mimic stone so well that buyers often can’t tell the difference

2. Cabinetry: Full cabinet replacement isn’t always necessary. Consider these strategic updates:

Cabinet refacing: About 30-50% cheaper than replacement while providing a completely new look

Paint and hardware: A professional paint job and modern hardware can transform dated cabinets for under $5,000

Selective replacement: Replace only the most visible or damaged cabinets while refinishing others

3. Lighting: Good lighting can make even modest updates look high-end:

Under-cabinet LED strips: Create ambiance and functionality

Statement pendant lights: Draw the eye and add contemporary flair

Recessed lighting: Brighten dark corners and modernize the space

Classic subway tiles in neutral colors offer an upscale look at an affordable price.Replacing an outdated sink and faucet can instantly modernize the kitchen.Paint delivers the highest return on investment of any single kitchen update.

Cost-Effective High-Impact Updates 1. Backsplash: Choose classic subway tiles or geometric patterns in neutral colors. They’re affordable but look upscale when properly installed.

2. Sink and Faucet: A deep undermount sink and professional-style faucet can give the kitchen a high-end feel without breaking the bank.

3. Fresh Paint: Choose warm neutrals or soft whites to make the space feel clean and inviting. Paint delivers the highest return on investment of any single update.

Where to Save vs. Splurge Save On:

Appliances: Mid-range, matching appliances often provide better ROI than high-end models

Hardware: Shop retail sales for cabinet pulls and knobs

Flooring: Luxury vinyl plank offers durability and style at a fraction of hardwood’s cost

Splurge On:

Professional installation: Poor workmanship can devalue even expensive materials

Quality faucets: They’re frequently used and scrutinized by buyers

Lighting fixtures: They serve as jewelry for your kitchen

The Numbers That Matter Based on recent market data:

Minor kitchen remodel average cost: $23,452

Value recouped at sale: 77.6%

Sweet spot budget range: $15,000-30,000

Avoid Common Mistakes

Don’t over-customize: Keep updates neutral and broadly appealing

Skip trendy choices: They can quickly date your kitchen

Maintain proportion: Ensure updates match your home’s overall value 4. Consider your timeline: If selling within a year, focus on visual impact over durability

The Bottom Line The key to a successful kitchen update is understanding your market and your buyers. In most cases, you’ll see the best return by creating a fresh, modern look without going overboard on high-end finishes. Focus on clean lines, neutral colors, and quality materials in the mid-range price point.

Remember: The goal isn’t to create the most expensive kitchen on the block, but rather the most appealing one within a reasonable budget. This approach not only attracts buyers but also provides the best return on your investment.

Need help planning your kitchen update? Let’s talk about what makes sense for your home and market. Contact Krasi Henkel at 703-624-8333 today for a personalized consultation and market analysis.

The landscape of generational wealth transfer is undergoing a massive shift. Over the next two decades, baby boomers and the Silent Generation are set to pass down an astounding $84.4 trillion in assets, including real estate, financial instruments, personal property, and even pets and livestock. As a seasoned real estate professional, I’ve witnessed firsthand how this inheritance process can become an overwhelming and emotionally charged journey for many families.

The Inheritance Roadmap: Navigating with Wisdom and Care Here are five critical considerations when navigating an inheritance:

1. Open Family Communication: The foundation of a smooth inheritance process is transparent, honest communication. Initiate conversations about estate intentions early:

Locate and review important documents

Identify the designated estate administrator

Discuss the location of wills and trusts

Understand the family attorney’s contact information

Uncover details about potentially valuable collections (art, antiques, coins)

2. Sibling Harmony: When multiple heirs are involved, expectations management is crucial:

Have candid discussions about the inheritance

Set realistic expectations

Create a framework that prevents potential conflicts

Prioritize family relationships over material possessions

3. Objective Property Assessment: Approach personal property and inheritance with both sentiment and practicality:

Carefully evaluate what items truly hold value for you

Consider sentimental attachments objectively

Be willing to let go of items that don’t serve a purpose

Respect the memories associated with belongings without being overwhelmed

Establish a relationship with estate auctioneer(s)

4. Real Estate Strategy: Develop a comprehensive plan for inherited property:

Create a timeline for property assessment

Determine whether to sell or maintain the property

Budget for potential improvements or repairs

Consult real estate professionals for market insights

5. Tax and Legal Preparedness: Understanding the legal and financial implications is critical:

Consult with a tax professional

Learn about inheritance tax laws

Understand potential tax implications

Develop a strategy to minimize tax burden

Here are five critical pitfalls to avoid when navigating an inheritance:

1. Hasty Storage Solutions: Resist the urge to quickly box everything and store it away. This approach:

Leads to unnecessary expense

Creates logistical complications

Prevents proper sorting and decision-making

2. Home Clutter Accumulation: Avoid filling your personal space with inherited belongings:

Prevents home organization

Creates unnecessary stress

Delays necessary decision-making

3. Overreliance on Verbal Valuations: Never take valuations at face value:

Consult multiple experts

Get professional appraisals

Verify the true worth of items

4. Family Conflict: Prioritize relationships over possessions:

Communicate openly and compassionately

Be willing to compromise

Focus on maintaining family bonds

5. Procrastination: Time is of the essence:

Make decisions promptly

Address legal and financial matters quickly

Prevent complications from delaying action

Emotional Perspective: Honoring Memories

Inheriting a household is more than a financial transaction—it’s an emotional journey. Remember that your loved ones cherished these belongings, but memories persist beyond physical objects. Be kind to yourself and your family during this process.

Key takeaway: Things have no permanence. Some items are meant to be memories, not permanent possessions. Embrace the opportunity to honor your family’s legacy while creating your own path forward.

By approaching inheritance with preparation, compassion, and strategic thinking, you can transform a potentially stressful situation into a meaningful transition that honors your family’s memory and your own future.

Are you or someone you know stressing about what to do with inherited real estate? Reach out to Properties on the Potomac at 703-624-8333 today!

Buying your first home is an exciting milestone, but it can also be a complex process with many decisions to make. To help you navigate this important journey, here are five essential tips that every first-time homebuyer should consider.

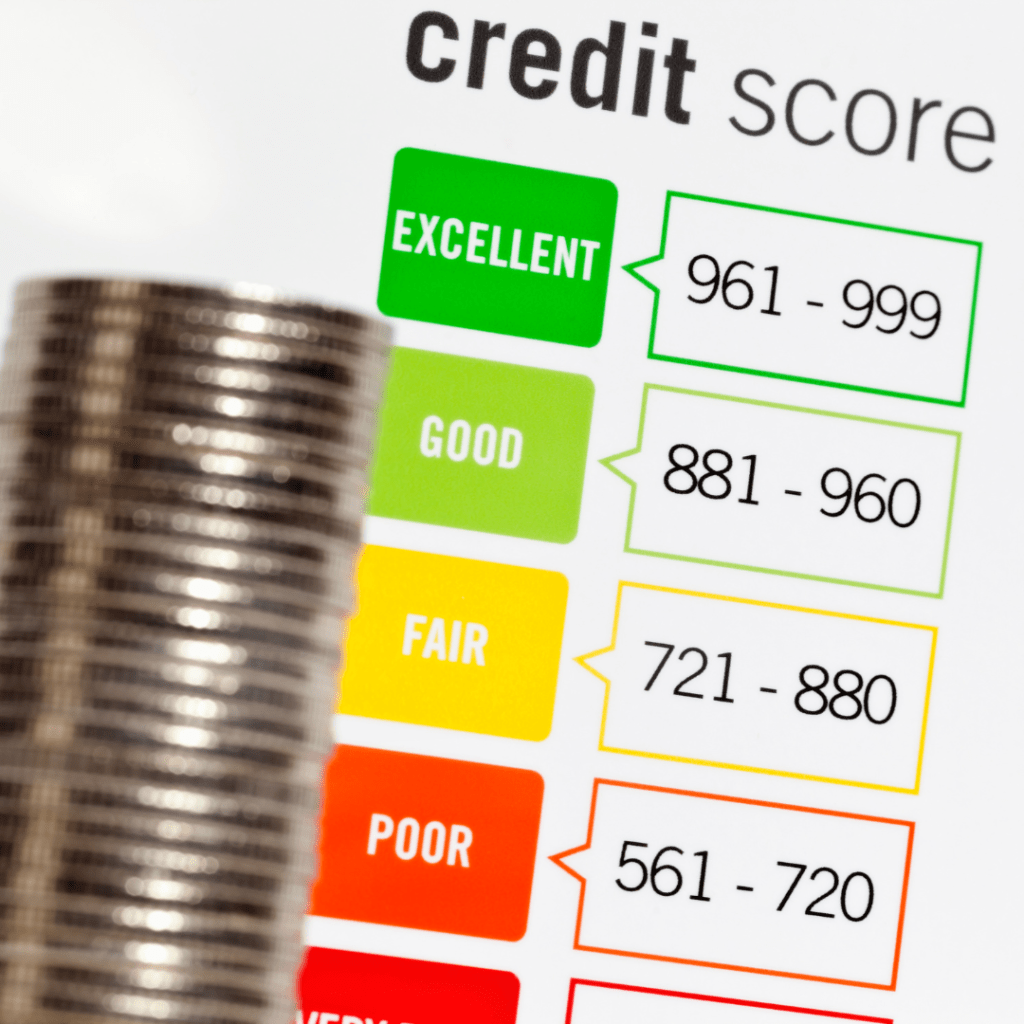

Check Your Credit Score Before you start looking at homes, it’s crucial to check your credit score. Your credit score will have a significant impact on your ability to secure a mortgage and the interest rate you receive. Lenders use your credit score to assess your reliability as a borrower, so a higher score typically results in better loan terms and lower interest rates. There are several different ways to check your credit online for free: annualcreditreport.com, through your credit cards, or creditkarma.com.

If your credit score needs improvement, consider paying down debts, ensuring bills are paid on time, and avoiding new credit inquiries. Small adjustments to your credit habits can lead to a big difference in your loan eligibility.

Get Pre-Qualified for a Mortgage Once you have a good idea of what your credit looks like, contact us at Properties on the Potomac. We can help guide you to the right lender so you can get pre-qualified for a mortgage. This process gives you a clear understanding of how much a lender is willing to lend you based on your financial situation. With pre-qualification, you’ll know the price range you can afford and avoid wasting time looking at homes outside your budget.

Understand Your Affordability Beyond the Mortgage Many first-time buyers focus solely on the mortgage payment when calculating affordability, but there’s more to owning a home than just the monthly mortgage. You also need to consider property taxes, homeowners’ insurance, utility bills, maintenance, and possible homeowners or condo association (HOA or COA) fees.

Compare Different Mortgage Options Mortgages are not one-size-fits-all. You’ll have options to consider, including how much you want to put down as a down payment (3%, 5%, 10%, 20% or more), fixed-rate versus adjustable-rate mortgages (ARMs), the length of the loan term—typically 15, 20, or 30 years. There are even different loan programs that can offer closing cost assistance.

Save for Upfront Costs While many first-time buyers focus on saving for a down payment, it’s important to also prepare for other upfront costs, such as closing costs, inspections, and moving expenses. These costs can add up quickly, so planning ahead will help avoid financial stress at closing time. Depending on the loan type, closing costs can range from 2% to 5% of the home’s value. Be sure to budget for these expenses to ensure you’re fully prepared when it’s time to finalize the purchase.

Buying your first home is an exciting yet challenging experience. By following these tips, you’ll be better equipped to make smart, informed decisions throughout the home-buying process.

Properties on the Potomac can help guide you through your next steps from start to finish. Whether it’s finding a top-quality lender or identifying the right mortgage option for your needs, we’re here to help. Contact us at 703-624-8333 today to start your journey toward homeownership with expert advice and personalized support!

We understand that buying a home is one of the most significant investments you’ll make in your lifetime. It’s not just about finding a place to live; it’s about finding your sanctuary. But making that dream a reality requires careful planning and diligent saving. Here are some essential tips to help you start saving for your first or next home.

1. Set clear and achievable savings goals. Determine how much you need for a down payment (it may be less than you think, contact us for more info), closing costs, and any additional expenses associated with buying a home. Having a specific target will keep you motivated and focused on your savings journey.

2. Create a budget and stick to it. Track your expenses and identify areas where you can cut back or eliminate unnecessary spending. Consider making small sacrifices now for the greater reward of homeownership later. For example, cut out automatic subscriptions/memberships, make home-cooked meals instead of eating out, or look for coupons/promo codes for everyday purchases.

3. Automate your savings. Set up automatic transfers from your checking account to your savings account each month. This way, you’re consistently contributing to your home fund without even thinking about it.

4. Explore ways to increase your income or generate extra cash flow. Whether it’s taking on a side hustle, freelancing, or selling items you no longer need, every little bit helps when it comes to saving for a home.

5. Take advantage of homeownership assistance programs and incentives offered by governments or financial institutions. These programs can provide valuable resources and support to help you achieve your homeownership goals more quickly.

6. Be patient and stay disciplined. Saving for a home takes time and requires sacrifice, but the reward of owning your own home is well worth the effort.

Ready to take the first step towards homeownership? Contact us at Properties on the Potomac at 703-624-8333 today to learn more about how we can help you find your dream home and guide you through the buying process.

Renting a storage unit can be a convenient solution when you need extra space for your belongings. However, there are some traps that renters often fall into when choosing and using a storage facility. Being aware of these pitfalls can help you avoid hassles and unexpected costs. Here are some common storage unit traps to watch out for:

Trap #1: Not Understanding the Contract Terms Before signing a rental agreement, carefully read through all the terms and conditions. Look out for things like administration fees, insurance requirements, late payment penalties, and restrictions on what you can store. Clarify anything you don’t understand to avoid surprises down the line.

Trap #2: Not Doing the Math Before contracting for a storage unit(s), look at what you plan to store. If you will be moving, will you want the things you plan to store? Cull out unneeded items and save money on the size of the unit you choose. That could mean several hundreds or even thousands of dollars in the long run.

Trap#3: Underestimating or Overestimating Space Needs Cramming a unit too full will make it hard to access your belongings. This can lead to damage and waste. Overestimating will lead to overpaying for unused space. Discuss with the storage company your space and items that you plan to store.

Trap #4: Poor Unit Condition When viewing units, inspect them thoroughly for any signs of moisture, pests, or structural issues that could damage your goods. Check that locks, lighting, ventilation, and security provisions are adequate. Don’t settle for a substandard unit.

Trap #5: Overlooking Climate Control If you’re storing valuables, paperwork, furniture, or anything that could get ruined by extreme temperatures and humidity, opting for a climate-controlled unit can prevent damage. Weigh the extra cost against potential losses.

Trap #6: Cheap but Inaccessible Sometimes the most affordable units are in inconvenient locations or have very limited access hours. Consider the hassle of getting to your stuff when needed. For frequently accessed storage, closer and more accessible may be worth paying a bit more.

Trap #7: Lack of Proper Insurance Most storage companies require you to have your own insurance to cover anything stored in their units. From the outset, look into getting the right coverage amount and type of policy to adequately protect your belongings.

By doing your homework and being aware of these common traps, you can steer clear of headaches and make sure your storage unit experience is a smooth, secure, and cost-effective one.

Are you planning to sell your house and thinking of renting a storage unit to offload excess belongings? Before putting in more work and expense than might be needed, contact Properties on the Potomac at 703-624-8333 now to discuss your staging needs.

Change is inevitable. With over 100 combined years in the real estate industry, we have seen changes in real estate practices and lending practices. The industry has demonstrated resilience because after all, we all need a home in which to live.

This week, as you have most likely read, The National Association of Realtors has reached a settlement regarding commission practices. The agreement is subject to legal approvals and much additional negotiation. We are closely monitoring these changes and will keep you updated.

Regardless of developments, our commitment to first quality service to you and our future clients will remain unchanged. Your satisfaction and success remain our top priorities. This is a great time to contact us with any questions.

Thank you for your loyalty.

Sincerely, Krasi & Tiffany Henkel Properties on the Potomac, Inc.